DATA AVAILABILITY REPORT Q4 2025

European DataWarehouse’s (EDW) Q4 2025 Data Availability Report provides semi-annual statistics on the outstanding number of active securitisations, loan amounts, and number of loans.

The latest report shows that the total amount of securitised loans and leases in our database is still very large and has stayed fairly steady, even though there are fewer deals than before. It also marks the shift away from ECB-format uploads to ESMA/FCA reporting formats, and the inventory helps users see which format was used.

As of Q4 2025, European DataWarehouse’s All-in-One Database (AIO) contains €888 billion in outstanding loans and leases across 16+ European countries, including the UK.

Market Concentration and Large Transactions

A smaller deal count is partly offset by an increase in the size of individual securitisations.

The largest outstanding securitisation is the French RMBS “BPCE Master Home Loans” with €94 billion, representing over 10% of total AIO volume.

- A smaller deal count is partly offset by an increase in the size of individual securitisations.

- The top 10 transactions together account for €285 billion, nearly one-third of all outstanding amounts.

- These very large deals typically originate from the largest lenders in each market.

However, not all lenders use securitisation, so securitised data may not always reflect full market dynamics.

In some markets, a single transaction dominates the entire asset-class universe; in France, BPCE Master Home Loans alone accounts for 60% of French RMBS outstanding.

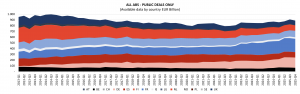

Geographical Composition of Securitised Data

Differences in securitisation usage mean that country shares in the AIO do not always reflect true market size (Exhibit 1).

- France: largest securitisation market with €232 billion outstanding.

- Germany: second with €178 billion.

- Italy: third with €110 billion, followed by the Netherlands and Spain with €93 billion each.

The latest major addition to the database is Wendelstein 2025 – 1, a German RMBS with €30 billion, now one of the three largest outstanding deals.

Exhibit 1: Amounts of Assets by Country

Source: European DataWarehouse

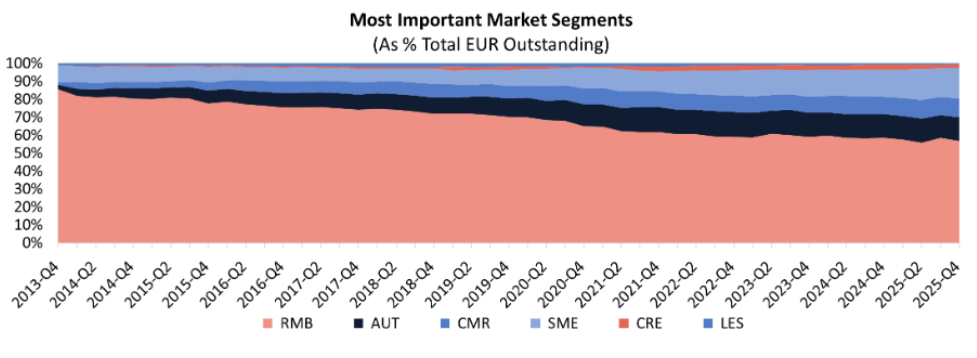

Trends Across Countries and Asset Classes

- Securitisation volumes evolve differently across countries and products:

- RMBS are present in most markets, but outstanding volumes have declined significantly, from a high of €870 billion in 2013 Q2 to about €500 billion since 2021.

- Germany: mortgage securitisations grew substantially—from <€30 billion in 2020 Q4 to €100 billion today.

- Netherlands: Dutch RMBS exceeded €200 billion until 2015 but are now roughly one-third of that level.

- Auto loans: amounts have been plateauing around €110 billion outstanding since 2022; Germany accounts for over 50% of all securitised auto loan balances.

- SME has rebounded strongly. From €100 billion outstanding in 2013 Q1, and after a low of €60 billion in 2018, SME outstanding has been steadily increasing towards nearly €150 billion. Spain has lost a lot of volume and there are no Portuguese deals left, but Italy and Belgium account for more than €30 billion each and France now accounts for €45 billion.

- Consumer loans: now account for almost €93 billion, dominated by Italy, and a substantial share of the growth has come from Spain, Germany and France.

- Leases: mostly, these have historically been leases to Italian SMEs. Italian leases declined from €16 billion outstanding in 2017 Q4 to about €5 billion.

- Credit cards: almost all of the amount outstanding relates to UK deals.

Exhibit 2: Share of Outstanding Amounts by Assets

Source: European DataWarehouse

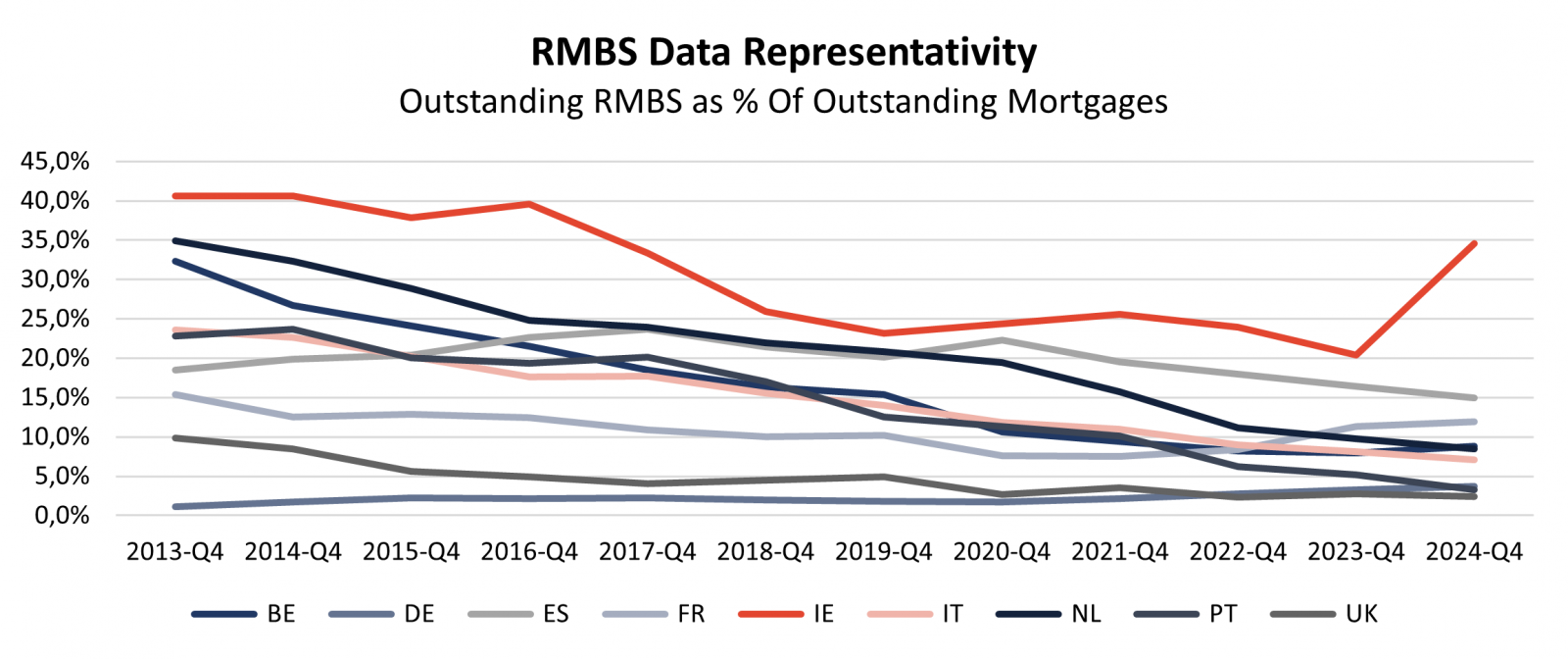

How representative is Our Loan-Level Data?

Exhibit 3 illustrates how representative our Residential Mortgages data is: the share of mortgages securitised as a percentage of total mortgages. The decrease in this ratio in most countries mirrors the drop in securitised mortgages already mentioned above. In Germany, the very small proportion of securitised mortgages reflects the preference for covered bonds. In Ireland, this proportion has always been high and increased further with the addition of one very large securitisation in 2024. The “deal by deal” tab of the data inventory makes it possible to monitor available data and related concentration effects.

Exhibit 3: RMBS Representativity (Securitised Share of Total Mortgages)

Source: European DataWarehouse; data from the European Mortgage Federation’s Hypostat 2025

Transition from ECB to ESMA/FCA Formats

The final dataset in ECB format was uploaded in September 2024. Going forward, all new submissions follow ESMA or FCA reporting formats. To support this transition:

- The Data Input tab identifies the reporting format for each dataset.

- An Overlaps tab highlights deals reported to both ECB and ESMA during the transition period, enabling format comparisons where fields differ.

Data Quality, Processing and Scope

The data used in this report is sourced from our All-in-One (AIO) Database, which consolidates ECB, ESMA, and FCA data in a harmonised structure. Key processing steps include:

- Adjustments for legacy errors (dummy values, decimal inaccuracies, inconsistencies).

- Currency conversion into euros where necessary.

- Exclusion of low-quality uploads (notably many pre-2013 Q3 submissions).

- For each deal, the report uses the latest available upload as of the end of each natural quarter (March, June, September, December).

Overall, EDW’s Data Availability Report Q4 2025 shows that the total amount of securitised loans and leases in our database is still very large and has stayed fairly steady, even though there are fewer deals than before. This matters because when there are fewer deals, a handful of very big transactions can have a bigger impact on the totals you see by country or asset class. Also, securitisation is used differently from one market to another, so the data doesn’t always reflect the full lending market, meaning comparisons work best when you benchmark carefully.

The report also marks the shift away from ECB-format uploads to ESMA/FCA reporting formats, and the inventory helps users see which format was used.

European DataWarehouse GmbH’s research team produces a number of annual indices and special research reports to highlight current trends in the European ABS market. The data set includes more than 4 billion loan-level data points from commercial mortgage-backed securities, residential mortgage-backed securities, small business loans, auto loans, consumer finance, credit cards and other ABS transactions.

Users can access the data on European DataWarehouse’s EDITOR platform to analyse and compare underlying portfolios.

Data used in this research is uploaded by ABS issuers to comply with European Securities and Markets Authority (ESMA), European Central Bank (ECB), and Financial Conduct Authority (FCA) regulatory requirements for asset-backed securitisation transactions.

For custom research reports or information on how to access the loan-level data yourself, please contact us at enquiries@eurodw.eu. Furthermore, if you have conducted research with our ABS data and would like us to feature it, please email us.

ACCESS COMPLETE EXCEL FILE NOW

|