MOTORCYCLE FINANCE: SEPARATING PHYSICAL AND CREDIT RISK

Motorcycles make up only a small share of the Auto ABS loan-level data available in European DataWarehouse’s datasets, but the sample still reveals interesting patterns in market size, brand mix, engine size and arrears performance.

In this blog, EDW examines a sample of motorcycle loan-level data from Auto ABS securitisations, which sometimes include motorcycles and scooters alongside cars. Consumer securitisations may also include them, but the reporting template for that asset class does not separate motorcycles from other vehicles.

To identify motorcycles reliably, the EDW research team used calculated fields developed for the Green Auto Securitisation project. These help separate motorcycles from cars and lorries when manufacturers or model names overlap, such as BMW, Honda, Suzuki, Mercedes and Renault.

Motorcycle present in EDW’S securitisation repository platform

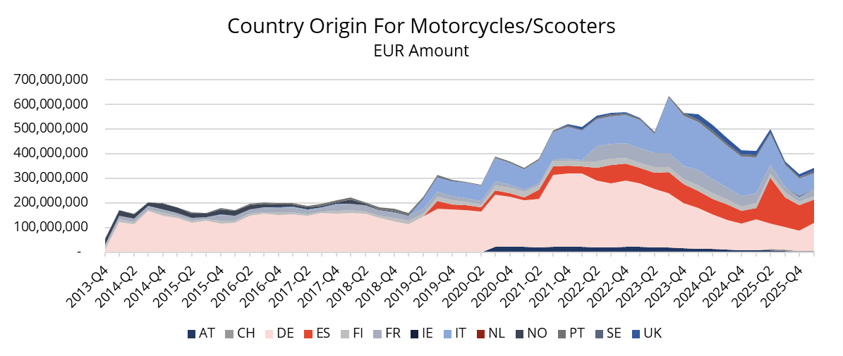

Motorcycle and scooter volumes in EDW datasets remain small relative to the full Auto ABS market, but rose sharply after 2020; there is possibly a ‘COVID effect’, as people purchased more bikes for commuting to avoid public transport.

Outstanding volume was below EUR 300 million before 2020 and reached about EUR 500 million between Q4 2021 and Q2 2024. Germany is the largest market in the sample, followed by Italy and Spain.

The market is highly concentrated. In Q2 2022, 36 Auto ABS deals contained at least EUR 1 million of motorcycle exposures, yet just five deals made up more than half of the outstanding amount. Most originators were non-captive lenders, with BMW’s Bavarian Skies programme representing the main captive exception.

Exhibit 1: Data Amount For Motorcycles in Our Database

Source: European DataWarehouse ; Amounts converted in EUR when applicable.

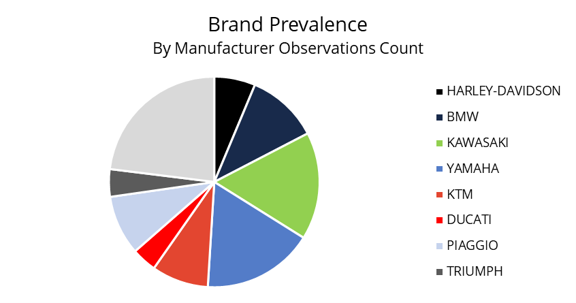

The brand mix in the database reflects securitised financing rather than the whole motorcycle market. Kawasaki and Yamaha are heavily represented, while Honda appears less often that it should, probably because it relies less on securitisation. Brands financed through consumer ABS cannot be isolated.

Exhibit 2: Motorcycle Brands in Our Database

Source: European DataWarehouse.

Kawasaki and Yamaha account for more than one third of the sample and lead by number of observations in Germany, Italy and Spain. Country patterns still differ: BMW represents 19% of German observations but is quasi absent from the Italian sample.

ENGINE SIZE DIFFERENCES ACROSS EUROPEAN MARKETS

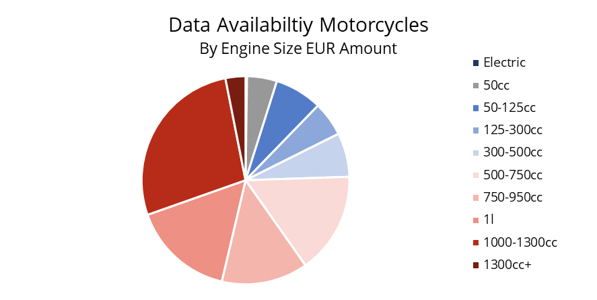

EDW has identified engine size for about 40% of the motorcycles and scooters in the sample. This was possible because engine capacity is often embedded in model names, while some models are associated with a single engine size. Electric motorcycles remain rare in the dataset.

Germany has the highest proportion of larger bikes in the sample (Exhibit 3). Half of all identified motorcycles have engines of 1 litre or more, compared with 20% in Spain and just 6% in Italy. At the other end of the spectrum, motorcycles below 500cc account for 22% of the German sample, versus 39% in Spain and 49% in Italy.

These differences likely reflect varying use cases. Smaller motorcycles are often purchased for everyday transport, whereas larger bikes are more commonly associated with leisure riding.

Larger motorcycles also tend to be more expensive and are therefore more likely to require financing. By contrast, 50cc mopeds represent only 1% of the total sample.

Exhibit 3: Identified Engine Sizes in Our Database

Source: European DataWarehouse.

FROM ENGINE SIZE TO CREDIT PERFORMANCE

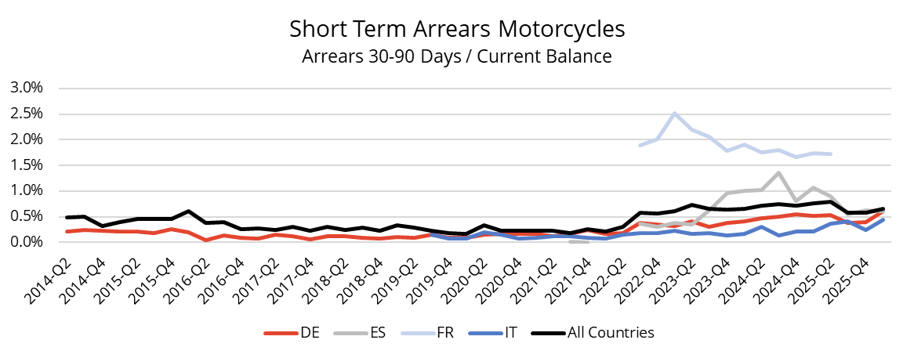

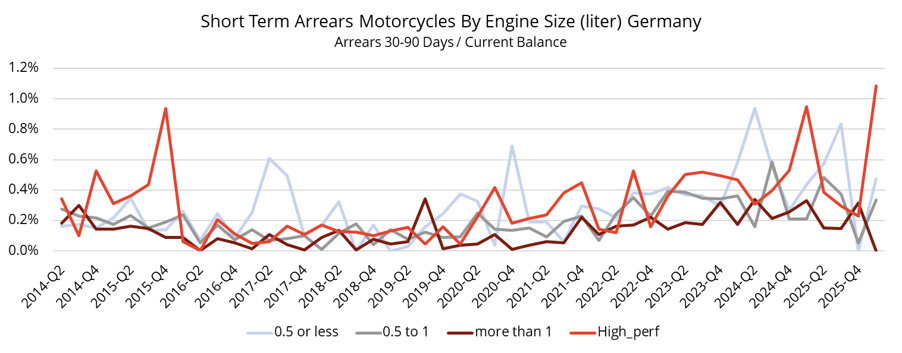

Short-term arrears have been rising in this segment. The strongest country-level data comes from France, Italy and Germany; Exhibit 4a shows 30-90 day delinquency indices only where at least EUR 30 million is outstanding. Before 2020, only Germany met that threshold.

Exhibit 4a: Short term Arrears Are on an Increasing Trend

Source: European DataWarehouse.

Source: European DataWarehouse.

One recurring finding from the GAS project is that delinquency rates tend to be highest for larger, more polluting automobiles. It was therefore worth examining whether a similar pattern exists in motorcycle finance, and Exhibit 4b is interesting in this respect.

To explore this, the EDW research team split the German sample into four groups: below 500cc (commuter bikes), 500cc to 1 liter (entry level bikes), above 1 liter (for seasoned drivers), and a separate high-performance category, which includes motorcycles with exceptional power-to-weight ratios and higher associated riding risks.

Exhibit 4b: Arrears are Highest For High Performance Motorcycles

Source: European DataWarehouse.

The sample is small (Exhibit 4b), but the overall pattern is clear. Motorcycles above 1 liter, excluding high-performance bikes, show lower arrears. High-performance bikes perform worst, although in terms of size and price they fall within the 1l category. The 500cc to 1 liter segment sits between the two.

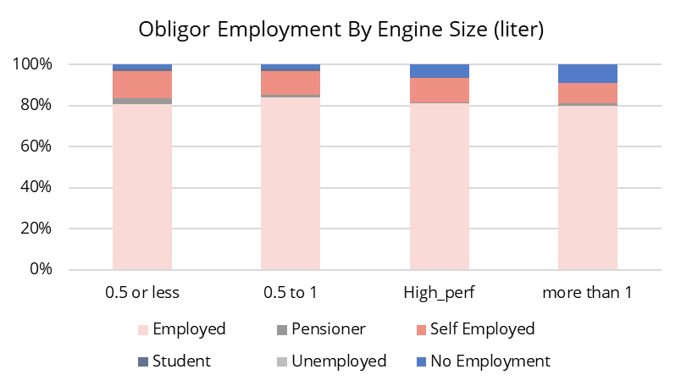

Exhibit 5: Employment Type vs Engine Size

Source: European DataWarehouse.

In terms of borrower profile, there is very little difference across categories, with employed and self-employed accounting for the vast majority of motorcycle purchases across categories (Exhibit 5).

Overall, the level of arrears for motorcycles are not actually very high compared with those observed for e-bikes or automobiles for the same index. This is possibly due to motorcycles being rather affordable vehicles, with prices of even high-end motorcycles falling within the same range as the smaller automobiles. However, the weaker performance observed in the highest-risk motorcycle segment suggests that physical risk may also be a contributing factor in credit performance.

Stay up to date with securitisation research trends by registering for one of EDW’s Research Update Webinars or get in touch via enquiries@eurodw.eu